Okay, so I’ve been meaning to get a new ride, something sporty, but, like, my insurance agent is practically family, and I didn’t want to see him faint when I told him my choice. So, I started digging into which sports cars won’t break the bank when it comes to insurance.

First, I made a huge list. I mean, everything that looked remotely fun and had at least two doors went on it. Then came the reality check.

Narrowing it down.

I started calling around, getting quotes. Let me tell you, that was a long process. I pretended I already owned some of these cars, just to get a realistic number. Some of those quotes, whew, I could have bought another used car with that money!

- First step: Online quote tools. They’re okay for a ballpark, but I found they weren’t always super accurate.

- Second step: Calling actual insurance companies. Yep, old school. This is where I got the real numbers.

- Third step: I put them into Excel and began comparing which cars were consistently showing lower quotes.

It was tough. One minute I was dreaming of open roads and roaring engines, the next I was staring at spreadsheets and insurance jargon. Talk about a mood killer!

I talked to my buddy who’s a mechanic, and he gave me some good tips.

He said that cars with good safety ratings and readily available parts are usually cheaper to insure. Makes sense, right? Less risk for the insurance company, lower premiums for me.

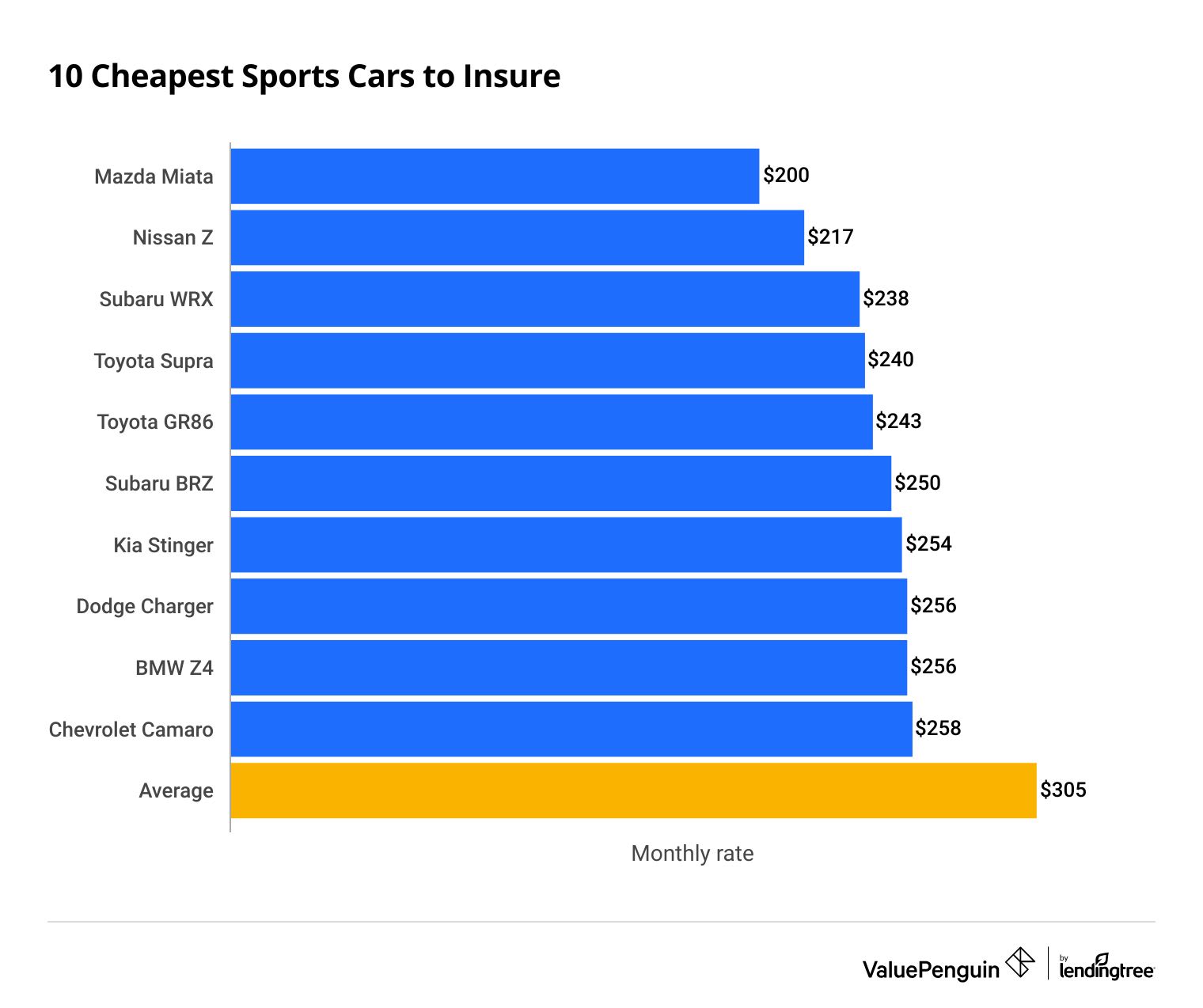

After all that,I have managed to pick a few cars.

But I am still thinking about which one to get.

{kind=link}